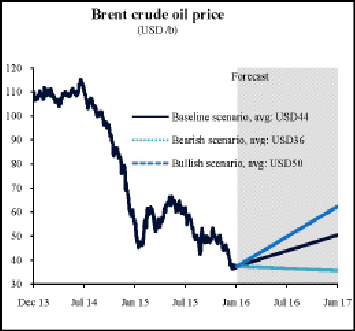

DOHA: Oil prices are expected to average $44 per barrel in 2016. A more bearish scenario, in which demand growth is more subdued than the baseline while supply growth is more robust, will result in oil prices averaging $36/b. A bullish scenario could lead to oil prices averaging $50/b, QNB said in a research note yesterday.

The banking major’s analysts noted recent turmoil in the oil market is evidence that they are notoriously hard to predict. The markets have been over-supplied since the beginning of 2014. Low prices are encouraging higher energy consumption and also pushing high-cost suppliers out of the market. “Under our baseline view of continued demand growth, US supply cuts, higher Iranian exports and sustained production from the rest of Opec, we expect the Brent crude oil price to average $44/b in 2016,” it said.

Oil markets are currently over-supplied by around 1.6m barrels b/d. Four questions are likely to determine how this excess supply will be cleared and therefore shape oil markets in 2016. First, will the strong demand growth persist into 2016? Second, how will the high-cost US shale producers respond to low prices which are making some of their businesses unviable? Third, when will the sanctions on Iran be lifted and how much more oil can Iran produce once they are lifted? Fourth, will the rest of Opec continue producing at current levels or will geopolitical factors disrupt their production?

To assess how these questions will impact oil prices, QNB considers three scenarios. Each scenario gives a combination of views on the four questions. Under the baseline, QNB forecasts oil demand to rise by 1.2m b/d in 2016, in line with the International Energy Agency (IEA).

QNB also assume that US shale oil production will be reduced by 0.4m b/d as some high-cost producers are driven out of the market. “Consistent with the IEA, we assume a gradual ramp up in Iranian oil production, with Iran ultimately adding 0.6m b/d to global oil supply by June 2016. Finally, we stipulate that that Opec’s crude oil production — excluding the additional Iranian supply — will be maintained at current levels of 31.7m b/d,” QNB said.

Under this scenario, the excess supply in the market is likely to be reduced to 0.8m b/d. Based on the historical relationship between changes in excess supply and oil prices, we expect oil prices to average $44/b in 2016,down from an average of $54/b in 2015.

The bearish scenario assumes a more subdued demand growth of around 0.9m b/d, equivalent to that of 2014. Under this scenario, the market imbalances will widen and excess supply will increase to 2.2m b/d. As a result, oil prices are expected to average $36/b in 2016, a decline of nearly a third compared to the 2015 average price. The bullish scenario stipulates that the strong 2015 demand growth of 1.6m b/d will persist into 2016. US supply is assumed to be cut by a more-than-expected 0.6m b/d.

Iran is assumed to add only 0.3m b/d by end-2016. The market will rebalance in 2016 with demand outgrowing supply by 0.3m b/d. As this starts to work out the large inventories built up over the last couple of years, oil prices will average $50/b in 2016.

The Peninsula